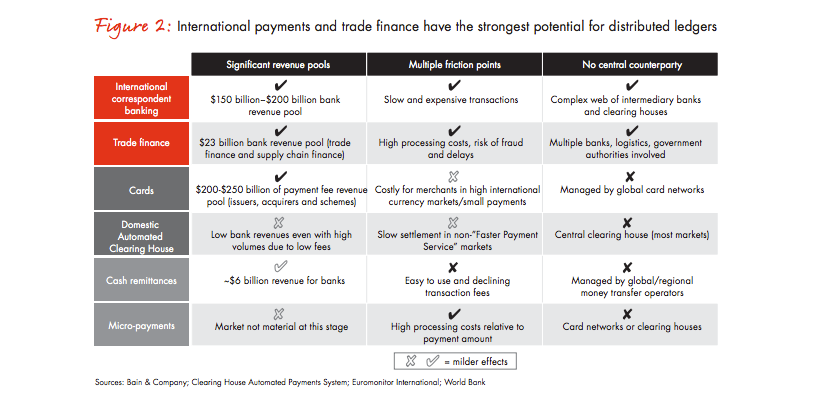

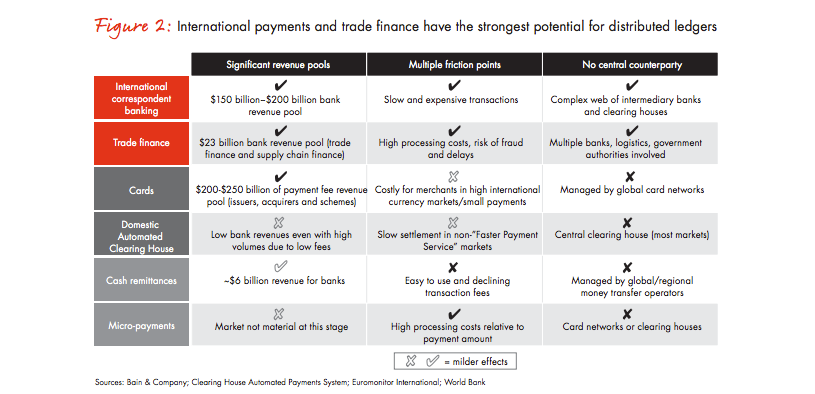

Image courtesy of Bain & Company.

Ripple Insights recently had the pleasure of talking with David Gunn, a partner at Bain & Company, and co-author of a recent Bain Insights report focused on separating blockchain hype from reality. Gunn shared his thoughts with us on the future of this technology and what banks should be focused on as it develops. Ripple Insights: In a recent report (“Distributed Ledgers in Payments: Beyond the Bitcoin Hype”), you reference how roughly $1 billion in capital has poured into hundreds of distributed-ledger investments since 2012. Is this just hype or are there real implications for banks? David Gunn: There are real implications for banks. In the area of payments the most relevant use cases in the near-term relate to international transactions. This is where the benefits of the technology have the greatest potential to improve services for customers by addressing significant pain points.

The attractive profit pools also stimulate focus from industry and technology players. This can fundamentally change the competitive landscape for the banks who benefit from the current correspondent banking networks. If distributed ledgers-based ‘fiat’ currency is adopted (with support from central banks), domestic payments come meaningfully into play. Cards and automated clearing house value chains could ultimately be superseded by true digital transactions – C2C, C2B, B2B.

The implications for banks can be profound, if they cease to control consumers’ primary electronic payment methods (cards and ACH), losing a critical part of the service they provide to customers, and weakening their customer relationships. RI: In your report, you said that piecemeal development of blockchain technology use will eventually give way to broad disruption of our financial system. Which use cases do you see as the most promising starting points or proving grounds for this technology, and why? DG: The most promising use case in the short term for payments is international transactions (underpinned by correspondent banking today).

This use case has high friction for customers and is costly for banks due to the lack of a central intermediary. Distributed ledgers concept can address this. Domestic payments in most markets are supported by a trusted central intermediary and generally work effectively today for a reasonably low cost.Consequently,, the hurdle a new distributed ledger-based payment mechanism must climb over is higher – in terms of improvements to payor/payee experiences and reduction of cost/price to the parties involved. The successful adoption of this technology is possible through banks which are attracted to this large profit pool and will be incentivized to invest the money and time required. This is evidenced by recent announcements on trials being run by networks of banks for this purpose. As they refine the technology this creates confidence among central banks to move ahead and potentially launch distributed ledger based fiat currency to reduce payment infrastructure costs and improve services to customers while enabling better level of monitoring and control.

RI: With such strong use cases in international correspondent banking, what’s holding back rapid change? DG: International correspondent banking is a network effect problem. Multiple banks are required to participate and invest in this to achieve scale which requires cooperation and a clearly-set objective. A strong collective agreement, among only a small number of banks, to make the concerted effort to establish standards, agree approaches to major sticking points (e.g. privacy, underpinning technology choices) can unblock this quickly. Early adopters will be part of networks which create a viable distributed ledger platform for international payments. Once this network achieves scale, there is little incentive for the participating banks to make it a completely open network to ensure that they can capture the profit pools.

For new entrants this is a lost opportunity, but for incumbents this can be a significant threat to a large existing profit pool. For domestic payments, even if it will take time for digital fiat currencies to emerge, there are other forces at work which banks must react to. Near-term threats for banks must be defended to avoid weakening payment relationships even before the advent of distributed ledgers – for example PSD2 in Europe, and the growth of third party alternative payment methods (e.g. Mobilepay in Denmark). Losing control of consumer payments relationships now weakens the banks’ ability to react to distributed ledgers in the future.

Image: Bain & Company report Distributed Ledgers in Payments: Beyond the Bitcoin Hype

RI: Many compare banks’ reluctance to adopt distributed financial technology to the slow adoption of mobile and online banking. When considering the Internet of Value that’s being built today, do you think the comparison is fair? Is this as fundamental a change as that was? Could it be even bigger? DG: Yes and no. There is certainly potential for massive disruption in the years to come, but the speed of change (and therefore the speed of reaction required) is not uniform. Distributed ledgers’ impact on domestic payments may still be years away, and it’s hard for banks to respond to what remain concepts rather than well-defined choices. For the more forward-looking banks there are opportunities to experiment, but for others the critical issue is having a clear view of how the market is evolving, and knowing when to move from ‘watching brief’ to rapid strategy development and execution as the future becomes clearer. For international payments, the comparison is valid. It is already clear that distributed ledgers can resolve old pain points, allowing much better customer experiences, and that new entrants are capable of entering the market and taking material share (e.g. Transferwise in remittances, albeit this isn’t yet based on the technology). For banks who currently generate significant revenues from the existing correspondent approach, it is critical they have a robust strategy to improve their service, or risk having the revenues taken from them. RI: Your report advised banks to accelerate their investment in digital wallets and payments apps. Why? DG: Banks rely on strong customer relationships for their business models. Payment services, even if generating only a small proportion of revenue, are critical to these relationships as a fundamental service the bank provides, and loss of these services can severely weaken banks’ relationships with their customers. The current wave of change, preceding distributed ledgers, is seeing payments shift from physical cards towards mobile equivalents (Applepay, AndroidPay), along with emergence of non-card payment types facilitated by mobile and ACH/account-to-account transfers. The latter is strongly encouraged by recent regulation in Europe – PSD2. Who provides these services is the key question for banks. If they are able to retain their position in the value chain as the primary consumer payments provider, it will position them well for a future underpinned by distributed ledgers (rather than cards or ACH). If, alternatively, the banks lose the battle and other third parties capture the consumer payment relationships, the banks will already be on losing ground as distributed ledgers become a reality. RI: What’s the most exciting thing about this shift in financial infrastructure towards the Internet of Value? And what main piece of advice do you offer banks who are currently weighing their options? DG: The excitement is the potential to create fundamentally better payment offerings for customers based on a new technology, eliminating pain points and inefficiencies which have existed for decades and even centuries. Fast-moving, innovative players can come out as winners through the transition; slower-moving players will lose out as the market landscape shifts. Our advice for banks is to review how prepared they are for this new technology, articulate what they stand to gain or lose in terms the business understands, and have a clear strategic view of where to invest heavily, where to experiment, and where to wait. Where there is much to be gained or lost, individual banks then need to move decisively to partner up, to resolve the technical challenges, and create momentum within the organization to help drive change.

David Gunn is a partner at Bain & Company. This interview is part of our series on leaders in our industry. For more like this, please subscribe to Ripple Insights.