Across the global payments industry, user experience and modern interfaces have been prioritized to meet growing consumer demand for user-friendly digital-first banking services. But the underlying infrastructure that moves money from one account to another has vast room for improvement, and the potential for blockchain and crypto to modernize the underlying payment rails has captured the attention of financial leaders around the world.

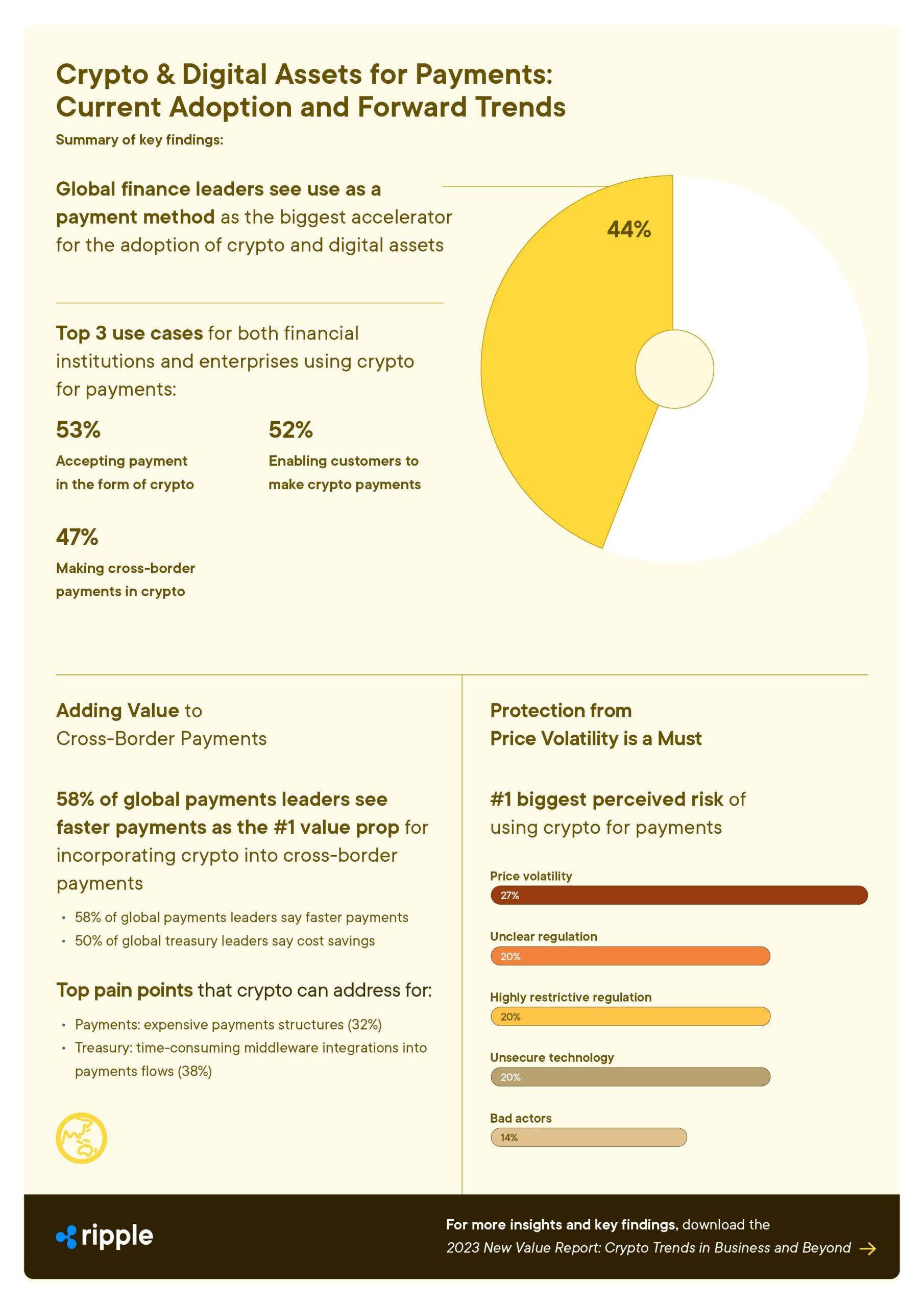

Ripple’s 2023 New Value Report reveals that 44% of survey respondents expect payments to be the biggest source of crypto adoption and nearly half believe cross-border payments is a top use case for crypto.

Payments, especially cross-border payments, still rely on legacy rails that can take days for transactions to fully settle. In contrast, blockchain and digital asset technologies provide a seamless global infrastructure in which payments can be sent and received anytime, anywhere, instantly with lower fees and 360 visibility.

Digital-first finance

Digital banking has witnessed a remarkable surge in recent years, empowering individuals and businesses with convenient access to financial services.

In the United States, over 65% of the population is expected to use mobile banking by 2025, driven in part by the popularity of open banking platforms and payment apps like Venmo and CashApp. Throughout Asia — the global leader in digital finance adoption — online banking is expected to reach nearly 1 billion users by 2024. In China, over 87% of respondents in an EY study have already used fintech services.

The total value of global mobile device payments reached $1.2 trillion in 2022, so it’s clear that much of the world engages with money and finance digitally first. While a remarkable shift in its own right, the highly designed user experiences that are drawing these customers in are actually masking outdated, fractured infrastructure.

Antiquated payment rails

Beneath the veneer of modern apps and services, transactions are still completed using traditional payment rails built decades before the internet and mobile phones. The complexity of legacy systems, coupled with the need for intermediaries to validate and settle transactions, introduces delays and inefficiencies, meaning money moves as slowly now as it did 50 years ago — despite the updated packaging that consumer-facing apps provide.

“Many (digital) platforms have created a really slick user interface that sits on top of a domestic payment rail. That means the actual funds aren't hitting the rails until a consumer is trying to cash out — and that transaction can take days,” explains Ripple’s Head of Payments Products Brendan Berry in an interview with PYMNTS.

“A lot of what we call innovation in this space actually brings the consumer further away from underlying payment rails so that they get a fabricated or synthetic sense of improvement, without actually fixing the underlying infrastructure limitations themselves.”

Moving funds internationally is even more obstructed. Patchwork global regulations and compliance requirements, currency exchanges, time zones and limited hours all add logistical weight to an already slow and expensive process.

For example, an international wire payment using traditional payment rails can take up to four days to settle, and the average global cost of sending a remittance payment is an astounding six percent (6%). The world economy may seem like an always-online global marketplace, but traditional finance still operates on a 9–5, Monday-to-Friday, schedule.

Respondents to Ripple’s global survey reinforce these frustrations, with cost of payments and settlement speed being two of the most frequently cited challenges for enterprises making cross-border payments.

Crypto-powered payments

Cross-border payments are central to the world’s economy; powering international trade, underpinning complex supply chains, enabling corporate treasury flows and funding the operations of non-governmental organizations. The frictions inherent in these transactions today needlessly inflate the time and cost of each of these applications.

Fortunately, cross-border payments have emerged as one of the more powerful use cases for crypto and blockchain, thanks to their radical ability to facilitate interoperability between tokens or chains. Once two parties agree on the value of a transaction, a crypto-enabled payment moves the corresponding amount of digital assets between the appropriate chains. These assets can be moved in seconds on a blockchain, and then liquidated into fiat currencies to pay out via local rails for a faster, more affordable and transparent payment.

"The magic of how that all happens is because you're using a digitized or tokenized asset, and the flow allows you the ability to move funds quickly,” says Berry. "It's achieved without incurring the costs associated with needing to rely on different financial institutions as a middleman in the flow, removing parties from a normal construct of correspondent banking.”

The value of cross-border payments is expected to reach $250 trillion by 2027, and the advantages of global payments powered by crypto are readily apparent. Further, more than half of global payments and treasury professionals point to faster payments and cost savings as the top two reasons to incorporate crypto into their cross-border payments business.

“Blockchain has all the makings of a transformative answer,” says Doug Fritz, CEO of F2 Strategy, a wealth tech consulting firm. “It enables payor and payee authentication and translation of value within the same line of code.”

A seismic shift in finance

This shift is already well underway. More than 80% of global finance leaders expect to begin using crypto in their businesses in the next three years.

By addressing the limitations of traditional payments systems and combining technology and finance seamlessly, blockchain is actively paving the way for a new era of frictionless global payments. It can enable instant transactions for individuals, businesses and banks anytime, anywhere.

Download the New Value Report today to learn why global financial and payments leaders believe in the power of blockchain to unlock this new payments landscape and how financial institutions, regulators and businesses can work together to make it a reality.