This post was originally published in 2022 and has been updated as of May, 2024.

Modernized payment systems and financial services are gaining traction across North America as standardized messaging, secure data exchange, and interoperability take shape. Here, we examine how open banking, FedNow, and ISO 20022 have contributed to streamlining the financial landscape in this region.

Banks and fintechs across the region are leveraging alternatives to traditional payment experiences and adopting technologies for real-time payments use cases extending through B2B, B2C, A2A, P2P, G2C, and beyond.

Today, the dynamic of connecting various banking and payment card accounts is leading to more customized payments products, faster access to credit and financing, and greater financial control for individuals.

Research suggests that the global open banking market will eclipse $130 billion by 2028, driven by rising consumer and institutional preferences for digital payments. In 2022, the market reached $15.21 billion, but is set to expand at a remarkable 24.6% estimated CAGR due to the growing use of digital payments and mobile wallets.

Additionally, open banking solutions have skyrocketed across myriad industries like financial services, healthcare, retail, and insurance.

Open Banking 101

Open banking takes place when banks and financial institutions give customers and customer-approved third parties digital access to financial data.

These third parties are often able to initiate payments as well as download and easily share information on account balances, payments, transactions, investments and more.

There are a number of benefits to open banking, such as:

- Broadened revenue streams through new API-enabled products

- Improved customer personalization and satisfaction via increased touchpoints

- Strengthened relevance for financial institutions through diversification of client offerings

- Expanded data transfer capabilities in which competitive third-party providers can access bank account and transaction data through APIs

- Support for financial inclusion as a broader range of data points can be used to assess a customer’s creditworthiness

Customers who consent to share information within an open banking system give providers a better understanding of their needs, enabling streamlined payments solutions, personalized products and offerings, and better user experiences.

Early, but Eager: Open Banking Trends in North America

Europe and the United Kingdom have historically been the first-movers across open banking adoption, however, rising US-based support is underway. Account to account payments which represent 45% of all electronic payments are growing 280% year over year in the UK. In parallel, 71% of US consumers now say they’d like to make purchases or pay bills directly from their bank account.

The past year has seen an uptick in newsworthy open banking initiatives. Coinbase announced a partnership with an account-to-account infrastructure company to improve deposit and withdrawal experiences in Canada, the world’s third-most crypto-aware nation.

Welcoming open banking opportunities can result in a rise in competition and a downward pressure on margins, which drive traditional financial institutions to either find new revenue streams or new cost-saving measures. Companies harnessing the benefits of open banking — particularly those incorporating blockchain innovations — have the opportunity to address both issues.

While the impact open banking has on banks, credit unions, payment service providers, and legacy institutions must be considered, there is ample economic opportunity for consumers and the markets to which these institutions contribute.

Leaders at the Financial Data Exchange (FDX) — a nonprofit industry standards body dedicated to unifying the financial services ecosystem — report that open banking initiatives are thriving in the US. Last year, they estimated that over 30 million consumers had converted from credential-based access (ID and password) to the more secure, tokenized API access. Likewise, FDX leaders suggest network effect-led growth from open banking use is imminent in the US.

Two additional forces have supported the growth of open banking in North America: US consumer demand and increased regulatory clarity. In terms of consumer use, Visa notes that 87% of US consumers are using open banking to link their financial accounts to third parties, however only 34% are aware that they are using the technology.

So while open banking advances are broadly considered market-driven, patchwork regulatory frameworks and educational initiatives may be slowing adoption. In Canada, the expected establishment of a country-wide open banking regime remains delayed. Should these forces reverse, more innovation could quickly emerge.

Still, activities from industry vanguards point to open banking momentum. Mastercard recently introduced small businesses to its open banking platform which provides advanced analytics. When business owners give permission to access their financial data via open banking, lenders can use Mastercard APIs to apply cash flow, balance, and payment history analytics to transactions. With improved insights on liquidity, revenue, cash flow, and default risk, lenders can tailor offerings and SMBs with more competitive growth financing.

Importantly, this signifies supply and demand momentum behind an expanding range of spending, financing, and payment tools.

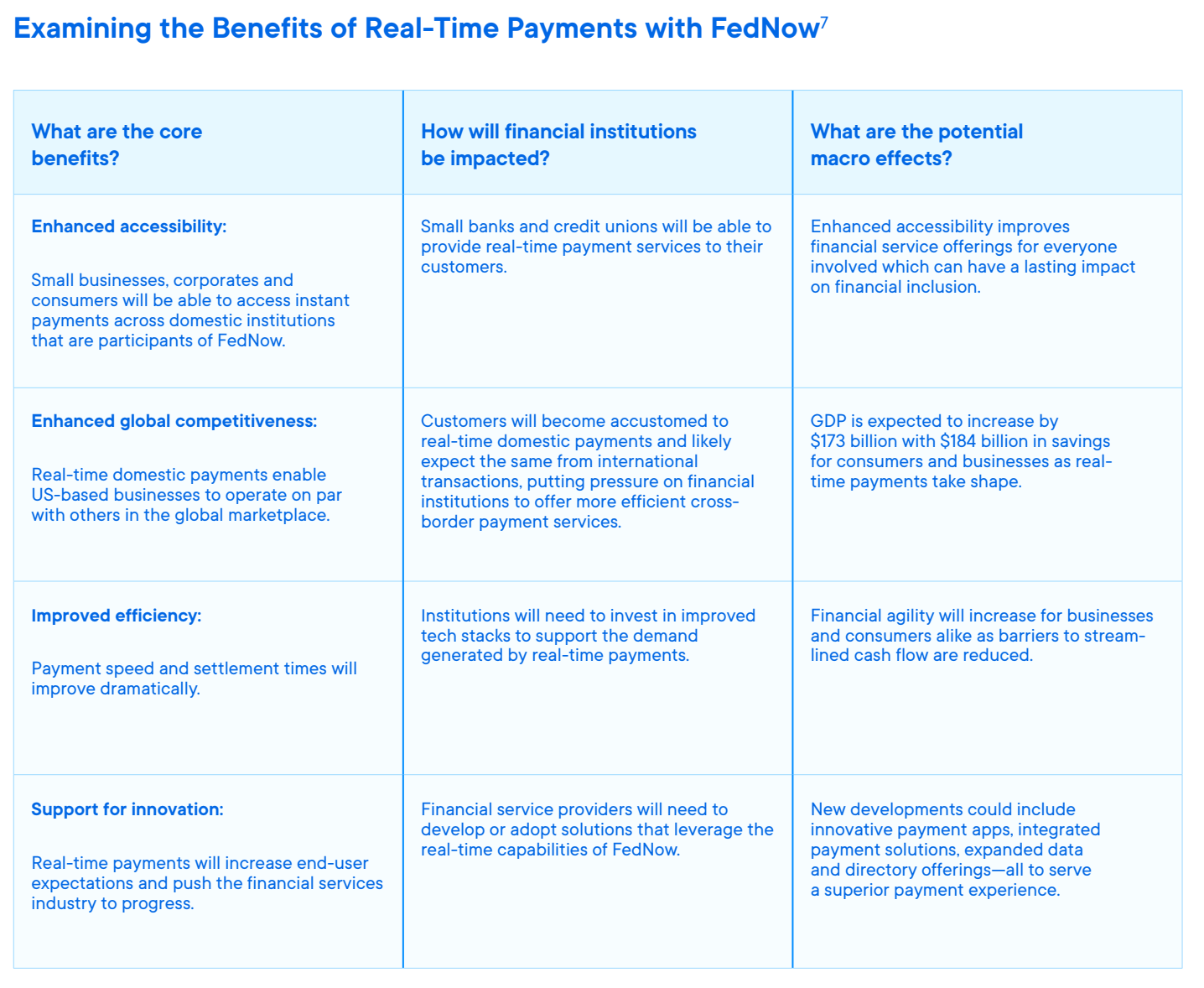

In conjunction, banking-wide system improvements like FedNow©, the Federal Reserve’s instant payment service, have allowed financial institutions of varying sizes to develop innovative solutions that can be personalized and data-driven to ultimately deepen customer relationships and strengthen brand loyalty.

FedNow® Launch and Impact

Towards the middle of 2023, the United States Federal Reserve launched the FedNow® Service to modernize the national payment system and enable faster, more efficient, and more secure domestic transactions.

The instant payment infrastructure is available to US-based depository institutions and allows individuals and businesses to send instant payments through institutional accounts.

While the RTP network was made available across the US prior to FedNow, the latter supports awareness efforts and helps grow adoption of real-time payment systems. As adoption and implementation expands, we anticipate a meaningful reshaping of the US financial landscape.

With this progress, financial institutions, fintech companies, and other stakeholders will have the opportunity to create new products and services that maximize the real-time capabilities offered through FedNow.

As customer expectations continue to rise alongside technological advances, depository institutions and their service providers can build on this capability and introduce value-added services to their customers.

Some 25% of financial institutions said they were waiting for FedNow to deploy before finalizing a real-time payments strategy, but major players in the payments space still haven’t moved on adoption. Taking a passive approach to innovation could be detrimental to an institution’s competitive stance as fintechs fill the gaps with more advanced offerings and global markets leverage progressive solutions.

FedNow will also leverage the ISO 20022 messaging standard, which is designed to be compatible with future iterations of the instant payments infrastructure.

ISO 20022 Goes Live

ISO 20022 serves as a universal language to more efficiently share financial data across the globe. The messaging standard represents the need for modernization and plays a critical role in supporting instant payment capabilities and expanding payment process innovations. ISO 20022 is expected to bring significant changes to how financial services are conducted, improving data quality and reducing errors across cross-border payment flows, while making transactions more efficient and secure.

Specifically, ISO 20022 offers a structured, data-rich common language for corporates and banking systems. This is necessary to move away from end-of-day batch file payments processing to real-time processing. The standard may also provide better analytics using more robust data elements, which could bolster financial institutions in generating new services and product offerings.

For corporates and financial institutions, ISO 20022 adoption will boost operational efficiencies, including the ability to exchange detailed remittance information with a customer payment. In addition, it adds support for straight-through processing and a reduction in errors and manual processing.

Growing adoption of the ISO 20022 messaging standard and the opportunity for highly structured data has led the Federal Reserve to incorporate the framework into its FedNow® service. According to the Federal Reserve’s bank services group, this standard will be able to support FedNow as it evolves and adds capabilities.

- An international standard for exchanging electronic messages

- Offers structured, rich data using XML syntax

- This format is already in practice for real-time, low-value and high-value clearing systems around the world.

- Offers richer references and improved remittance information

- Requires planning ahead: multi-year project for financial institutions to implement value-added services to enhance experience