Blockchain makes big promises. Like: distributed financial technologies can dramatically reduce or even disappear settlement costs. We did the math and while Bitcoin and other blockchain systems are a different story, Ripple can save banks up to 60 percent in costs associated with global interbank settlements.

The most exciting part of our analysis isn’t the savings. It’s what the savings enables - entirely new, future-forward transactional applications. Since 2013, we’ve talked about how Ripple lowers the total cost of settlement. Ripple allows banks to transact directly and instantly so they can service payments on demand.

Today, cross-border payments are processed through a chain of banks with each intermediary representing a potential point of delay, failure and cost. Smaller, respondent banks depend on large correspondent banks to provide liquidity for their cross-currency payments. The process requires respondent banks to outlay liquidity in nostro accounts with correspondent banks.

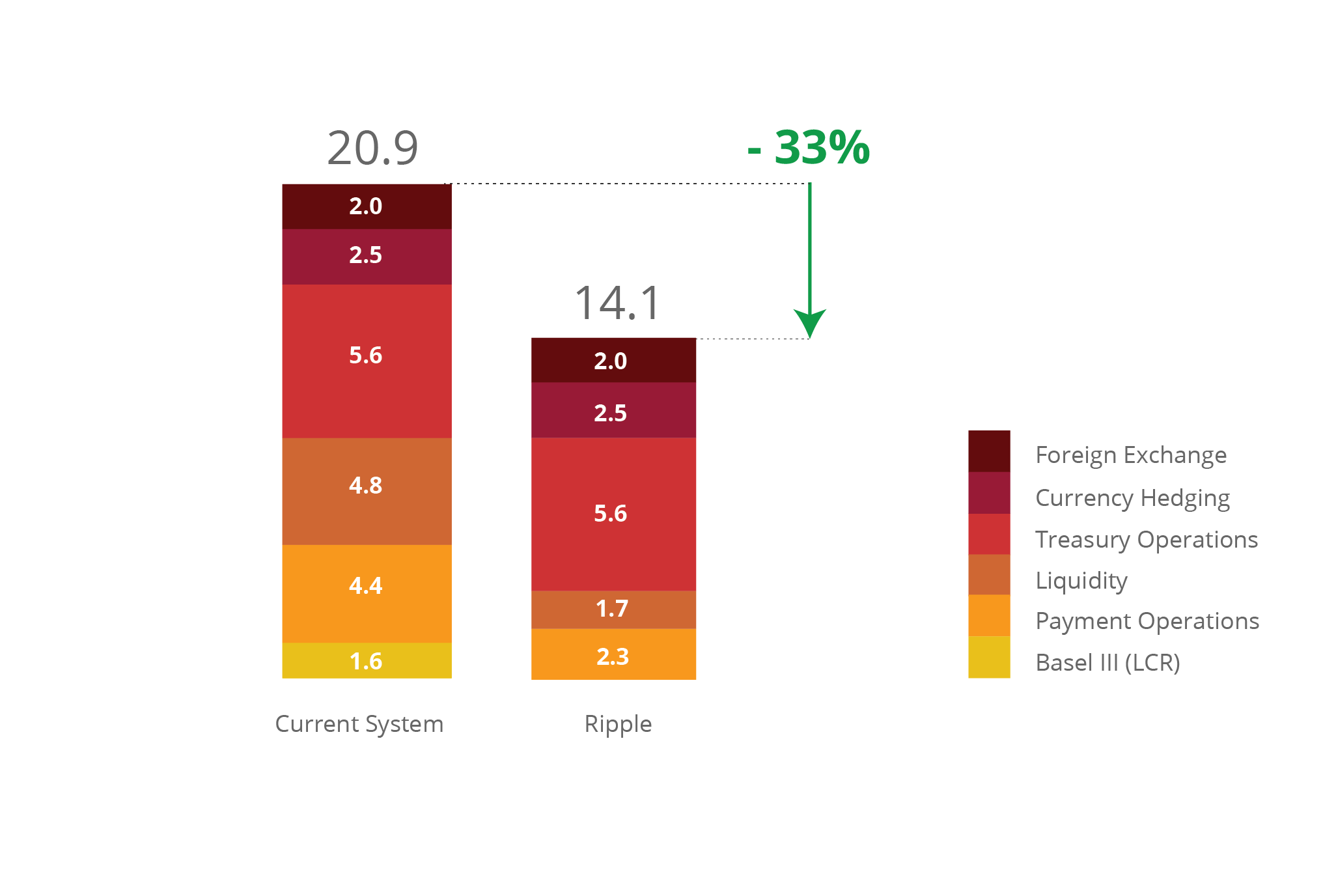

Correspondent banking costs make servicing certain types of cross-border payments, like low-value payments, unprofitable for banks. By matter of enabling instant, point-to-point settlement, Ripple reduces these liquidity requirements. And by matter of providing end-to-end visibility into each settlement, Ripple compresses payment operational costs associated with reconciling exceptions and failures. In The Cost-Cutting Case for Banks, we analyze the ROI of a representative respondent bank using Ripple. For this type of bank using Ripple as an infrastructure solution, it can save 33 percent in liquidity, Basel III and operational costs.

International Payment Infrastructure Costs

Global Average Cost: 20.9 bps on payment volume

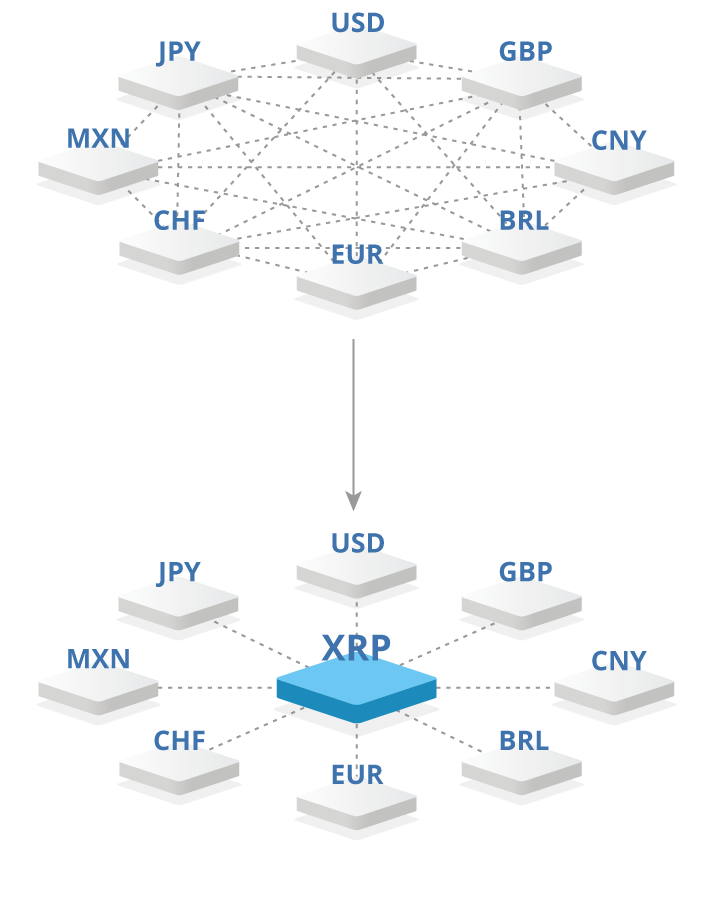

We then examine the cost structure for global interbank payments using XRP, the native digital asset to the Ripple consensus network, as a bridge asset. Like all digital assets, XRP is a store of value that can be transferred between parties anywhere in the world without a central counterparty. Uniquely, XRP can also support liquidity between any two currencies, acting as a bridge asset.

Instead of holding local currency in nostro accounts around the world, banks (or third-party market makers on their behalf) can consolidate their liquidity for global payments into one XRP account, held on their own balance sheets. This singular XRP pool then allows respondent banks to allocate less total liquidity to service the same volume of international payments in three ways:

- They only have to hold domestic currency and maintain one account with XRP versus many, expensive nostro accounts around the world.

- They only need enough XRP on hand to service their largest expected payment obligations, freeing previously trapped liquidity idling in nostro accounts around the world. XRP allows banks to access liquidity on demand.

- By making markets directly between their domestic currencies and XRP, banks minimize the number of intermediaries involved and their markup on spreads.

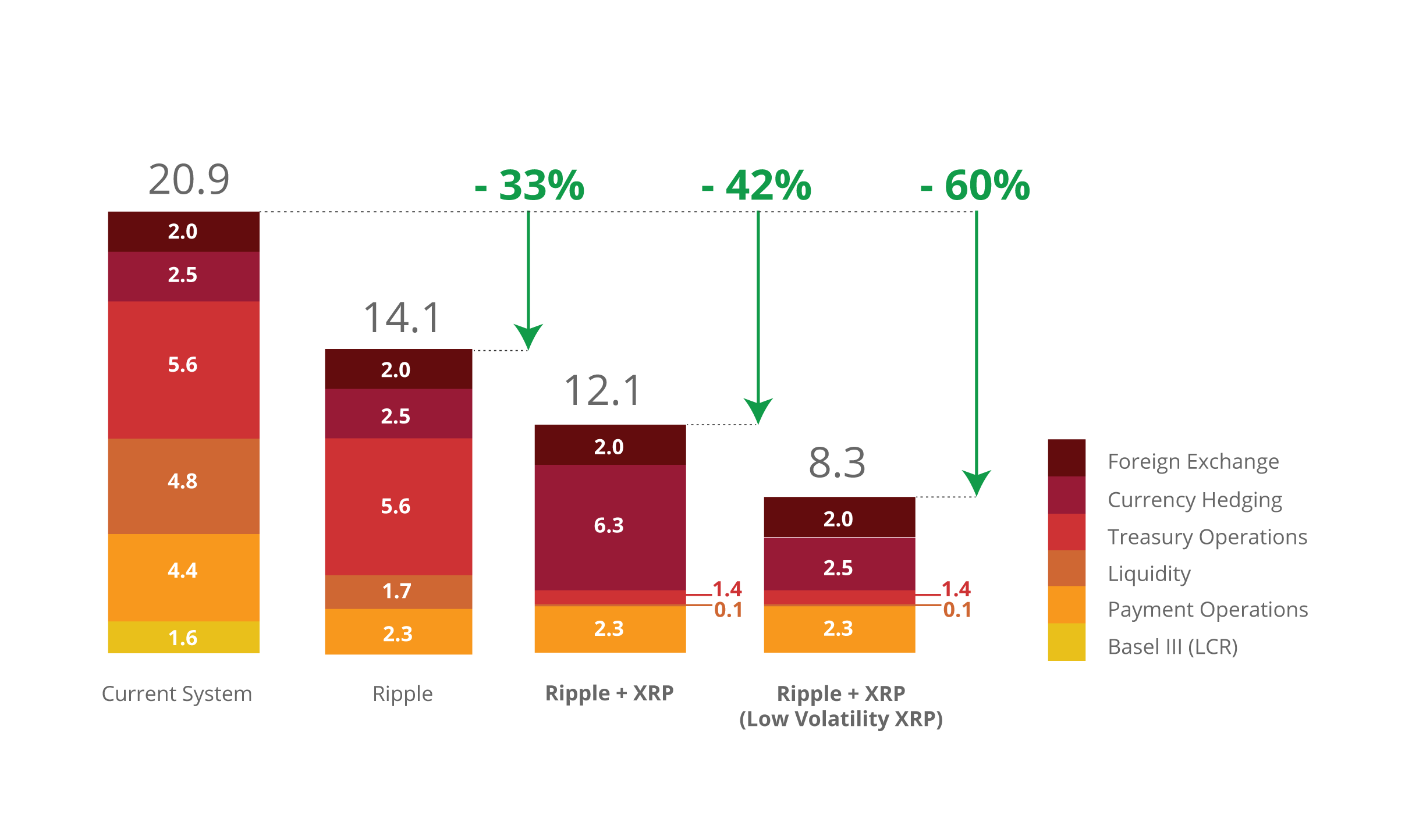

As a result, respondent banks that use Ripple with XRP as a bridge currency can save up to 42 percent on costs today and up to 60 percent as XRP gains usage and volatility decreases. To accelerate market thickness and reduce volatility for XRP, Ripple will soon introduce an XRP incentive program to algorithmically rebate market makers who provide liquidity through XRP.

International Payment Infrastructure Costs

Global Average Cost: 20.9 bps on payment volume

By matter of rewiring the world’s financial plumbing so transactional costs are a step change lower, distributed financial technology makes the currently impossible or improbable both possible and profitable. In the world of payments, a technology solution like Ripple and XRP creates unprecedented cost-efficiency and global reach, so banks can profitably serve use cases like global disbursements, international cash pooling, low-value remittances and even micropayments. Beyond payments, this same model of using Ripple and XRP can free billions of dollars currently trapped in collateral accounts or absorbed as costs in any other financial market from repo to derivatives.

The prescient banker doesn’t look at how she can make incremental improvements to today’s systems with blockchain technology, but how she can adopt today to position her bank to survive and thrive through the evolutionary change already underway.

Stay tuned on new developments with XRP at the XRP Portal.

XRP Newsletter