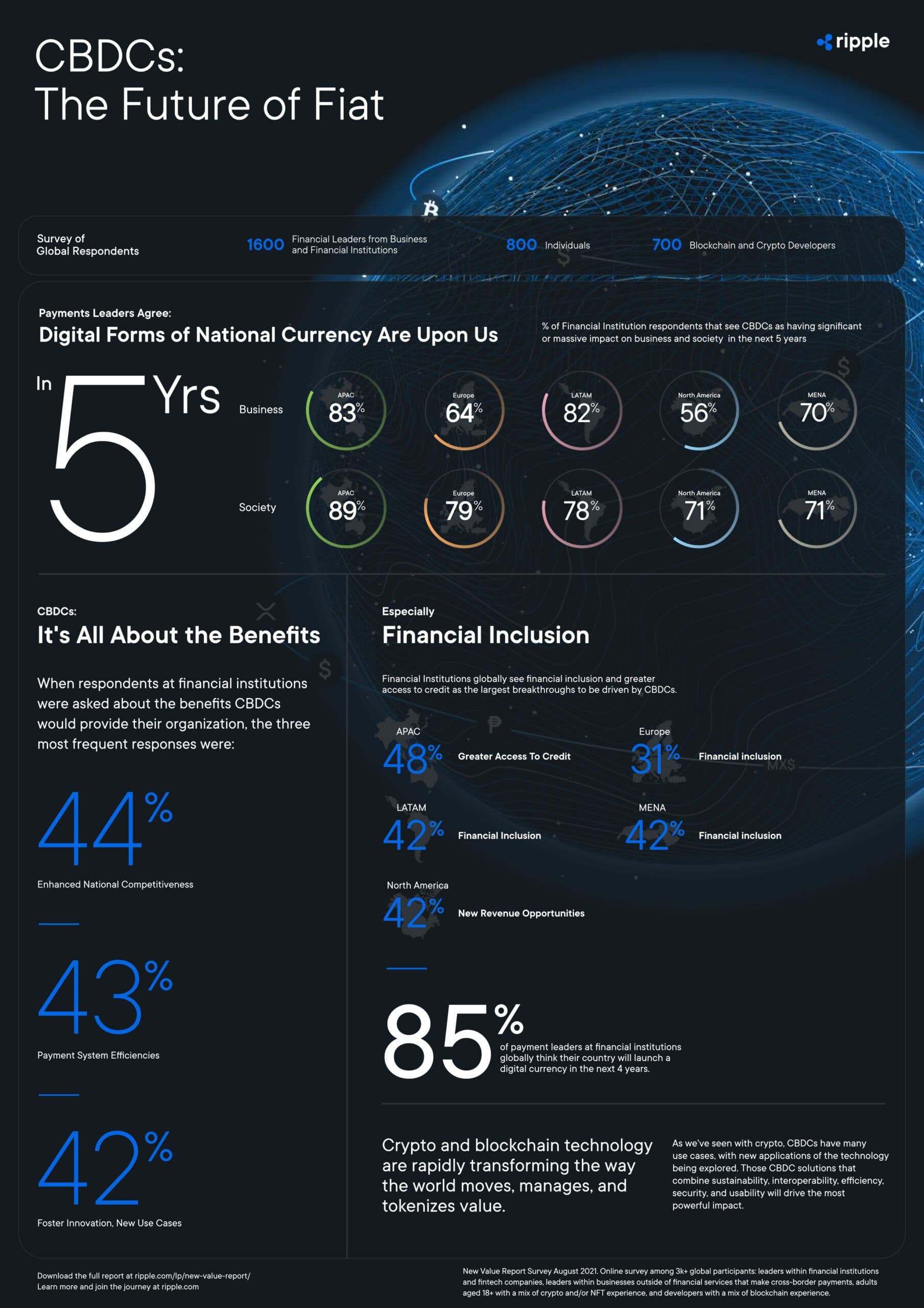

A visualization from Ripple’s New Value Report suggests the potential for central bank digital currencies (CBDCs) has generated an overwhelming consensus among financial institutions.

The new infographic highlights CBDC-specific takeaways from survey questions asked of 1,600 finance leaders around the world.

Financial Inclusion

More than 70% of respondents surveyed across five global regions believe CBDCs stand to deliver major social change within the next five years, with Asia Pacific ranking the highest at 89%. Specifically, four out of five regions see financial inclusion or greater access to credit as the largest potential breakthrough to be driven by CBDC solutions.

This shared belief is backed up by real-world CBDC initiatives. For example, Bhutan believes its ability to deliver more efficient and cost-effective payments using a CBDC – both domestically and internationally for things such as cross-border remittances – can help the country meet its goal to increase financial inclusion to 85% by 2023. Similarly, a new report from the International Monetary Fund reinforces the potential of the Bahamian Sand Dollar to advance financial inclusion for its citizens.

In addition to faster and more affordable payments, the digital nature of CBDCs can make loans and other financial services more accessible to historically underserved communities. This ability to more easily secure and repay loans could subsequently lead to more people establishing and building a credit history. A government-backed digital currency could also facilitate easier distribution of funds for social welfare programs, as seen with stimulus efforts in the recent pandemic.

Of course, there are real-world limitations standing in the way of broad CBDC rollout and adoption. Consumer education, identity verification, offline access, and privacy and security protections are all hurdles to implementation. Alternatives and solutions exist for these challenges, but they must be solved at scale and in agreement between countries to ensure interoperability among currencies.

Gaining Traction

Overall, delivering on the promise of this technology is more critical as CBDC projects around the world pick up steam. A survey by the Bank for International Settlements found that nine out of 10 central banks are now exploring CBDCs—up from 80% in 2021. The People’s Bank of China recently announced it would expand its pilot of the e-CNY to more cities, and Norway is testing its own prototype for a CBDC.

This tracks with another key survey finding highlighted in the infographic. Eighty-five percent (85%) of leaders at financial institutions think their country will launch a digital currency within the next four years. And beyond financial inclusion, many of them feel this technology would deliver enhanced national competitiveness (44%), greater efficiencies within their payment systems (43%) and advance innovation more broadly (42%).

Ultimately, consensus on the potential for CBDCs to bring about more inclusive financial systems is clear. While there remains much work to be done, many expect the transformation to be timely and that we will begin to see the fruits of this transition before the turn of the decade.

Want to play a role in the future of CBDCs? Apply now to enter Ripple's CBDC Innovate challenge—applications are open to all enterprise and individual developers through August 25.