For the last several years, most blockchain progress has focused on asset representation and transfers, issuing digital instruments, settling transactions faster, and reducing friction in value transfer.

But moving an asset onchain is only half the job. Real financial markets depend on what happens next: borrowing against assets, putting them to work as collateral, accessing liquidity without having to sell. That layer - lending and credit - barely exists onchain yet, and its absence is what stops tokenized markets from functioning like real capital markets

As more real-world assets move onchain, including treasuries, money market funds, stablecoins, commodities, and private credit, the question is no longer just whether those assets can exist onchain. It is: How do they become productive once they are there? How does a payment provider bridge liquidity between settlement windows? How does a market maker finance inventory without selling assets? How does an institution borrow against onchain holdings using terms its treasury and risk teams can actually evaluate?

That is the problem the XRPL Lending Protocol is designed to solve. In building the protocol, we made a deliberate choice to keep credit judgement off-chain, and standardize execution onchain. This is the core design principle.

The Missing Layer in Onchain Finance

Tokenization has made real progress. Assets that used to live only inside bank and fund admin systems can now be represented onchain.

The infrastructure to issue and hold an asset is fundamentally different from the infrastructure to finance against it. In traditional markets, those are separate systems. Custody and issuance live in one place. Financing - repo, margin lending, structured credit, working capital facilities - runs through another. That second layer is what makes assets productive, not just portable.

Most blockchain systems still blur those lines. A token gets issued. A lending application gets built around it. Another protocol creates its own borrowing rules, liquidation logic, and risk model. That was workable for early experimentation. For institutions evaluating credit activity, the result is a fragmented landscape, with liquidity scattered across isolated pools, credit behavior inconsistent across markets, and risk that must be re-underwritten protocol by protocol.

Building a durable credit layer requires treating credit as infrastructure, not as one more application layered on top of the network.

Why Credit Should Live at the Protocol Layer

Blockchains are good at enforcing rules consistently and recording what happened permanently. What they cannot do is make credit judgments - deciding whether a borrower is creditworthy, navigating regulatory requirements that differ by jurisdiction, or assessing collateral the way a lender would.

A blockchain should not replace credit teams, legal documentation, or institution-specific compliance frameworks. Those belong off-chain, where the judgment required to do them well can actually be applied. What the protocol can do is standardize what happens after a credit decision has been made: how liquidity is pooled, how loans are originated, how interest accrues, how repayment schedules are enforced, how defaults are processed.

Most onchain lending systems have conflated the two by building underwriting assumptions directly into protocol logic, which is where institutional usability begins to break down.

The XRPL Lending Protocol takes the opposite approach. Institutions handle the credit judgment off-chain, while the protocol standardizes execution once terms have been agreed.

What the XRPL Lending Protocol Makes Possible

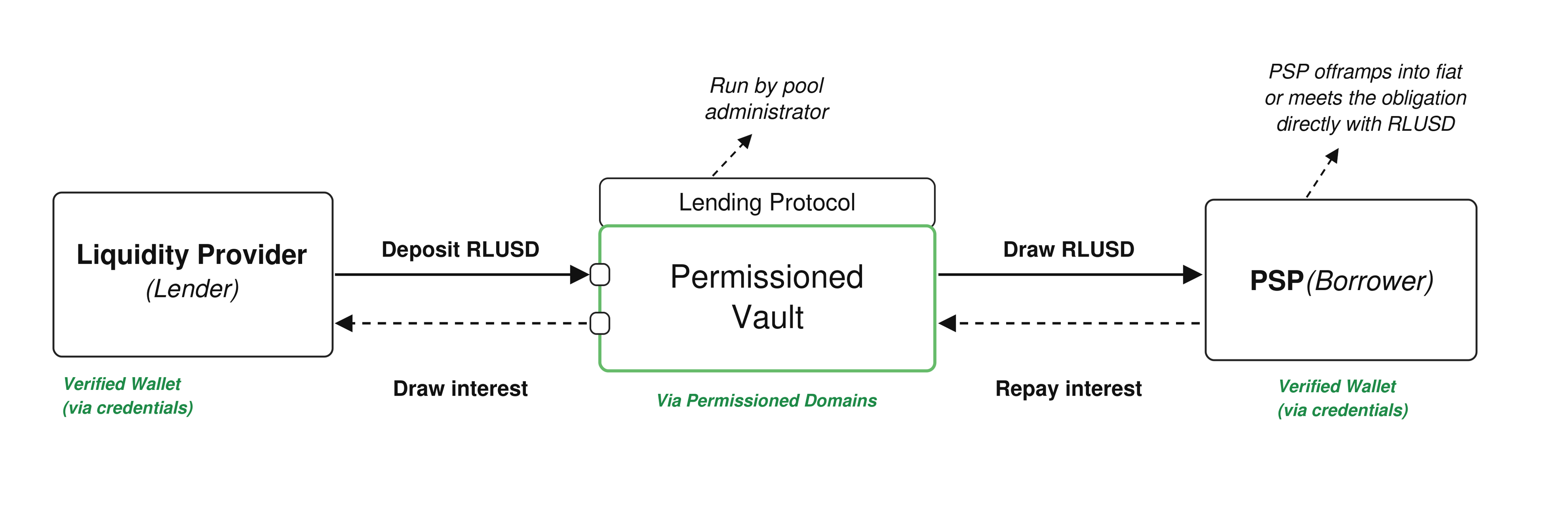

The XRPL Lending Protocol is built on two complementary components:

- Single Asset Vault — a standardized structure for pooling and managing a single asset onchain.

- Lending Protocol — enables that pooled liquidity to be originated into loans with defined terms, servicing, and repayment logic.

Together, they provide a foundation for onchain credit. The vault is where liquidity is organized, and the lending protocol is how that liquidity is put to work.

This separation mirrors real financial infrastructure. In capital markets, the container that holds assets is not the same thing as the mechanism that finances them. By preserving that distinction, XRPL can support a wider range of credit structures over time, rather than hard-coding one lending model into a single application.

Technical note: The Single Asset Vault and Lending Protocol are defined in XLS-65 and XLS-66, respectively, and remain subject to validator approval.

What This Looks Like in Practice

A payment provider holds RLUSD reserves onchain, but a cross-border settlement won’t close for another 48 hours. They need liquidity now to fund outgoing payments. Instead of drawing on an expensive bank credit line or selling assets at the wrong time, they access a short-term working capital facility through a licensed pool administrator, borrowing against expected settlement inflows.

The loan terms are agreed upfront. Repayment occurs according to those terms and is enforced by the protocol. There is no manual process, no governance vote, and no ambiguity around how the facility operates at maturity.

Before accessing the pool, both lenders and borrowers complete compliance checks. Once approved, verifiable credentials determine who can participate and under what conditions.

That is institutional-grade onchain credit, replacing a bank credit line that might cost 300-400bps with a facility whose terms are transparent, auditable, and enforced programmatically And it is the foundation for more: inventory financing for market makers, underwritten facilities backed by digital assets, and over time, more sophisticated structures, built on a common execution layer rather than rebuilt from scratch each time.

Built for Institutional Use

The XRPL Lending Protocol is designed around a simple principle: institutions retain control over credit decisions, while the protocol standardizes how those decisions are executed.

- Underwriting stays off-chain. Institutions already have credit teams, policies, legal documentation, collateral agreements, concentration limits, and regulatory obligations. The protocol assumes underwriting is done off-chain by the appropriate institution. Once terms are agreed, the blockchain enforces the mechanics. Credit assessment and credit execution are separate functions - and they should stay that way.

- Loan behavior is enforced natively onchain. Once a loan is originated, repayment schedules, interest calculations, and default conditions follow predefined rules. Risk teams, auditors, and regulators need to understand how a system behaves under both normal and stressed conditions - and standardizing those behaviors at the protocol layer makes it easier to evaluate, operate, and trust.

- Risk is structured, not socialized. The protocol supports first-loss capital at the facility level. Pool administrators or underwriters put junior capital at risk ahead of senior liquidity providers. Keeping losses contained at the facility level aligns incentives, enables risk-based pricing, and reflects how institutional credit markets are typically structured.

Why XRPL: Public Network, Protocol-Level Standards

Institutional credit markets require two things that have often been difficult to reconcile onchain: broad network participation and institutional-grade controls.

Public lending protocols - Aave, Compound, Maple, and Clearpool - demonstrated that onchain lending can operate at scale and attract meaningful liquidity. At the same time, many were designed around crypto-native governance models and risk frameworks that don't align with how institutions evaluate and manage credit risk. When a protocol changes its risk model, institutions have no reliable way to underwrite that change in advance - and that is not a manageable edge case. It is the core of how risk underwriting works.

Private and permissioned systems address many of those control requirements, but often do so by limiting participation to a closed set of counterparties. While that can create consistency, it cuts off the liquidity, distribution, and network effects that make public infrastructure valuable.

XRPL is designed to bring those capabilities together.

Credit infrastructure is standardized at the protocol layer rather than implemented through isolated applications with their own governance models and risk frameworks. The network remains public, allowing institutions to access broader liquidity and distribution while supporting permissioned participation through credentials when required.

Credit markets do not exist in isolation. They sit alongside payments, collateral movements, treasury operations, and settlement flows. XRPL has been handling institutional settlement at scale for over a decade. Building a financing layer on the same network that supports those activities reduces operational complexity and allows institutions to manage more of the financial lifecycle in one place.

What This Unlocks

The lending protocol matters not because it creates another yield product, but because it makes digital assets more productive. It gives institutions a way to treat onchain assets as working capital rather than static inventory.

- A payment provider can access short-duration liquidity to bridge settlement timing gaps.

- A market maker can finance inventory without selling core assets.

- A treasury team can deploy idle digital assets into underwritten facilities with clearer terms and risk allocation.

- A lender can build structured credit products on top of a common infrastructure layer instead of building a custom protocol from scratch.

Beyond Tokenization

The next phase of blockchain in finance will not be defined by whether an asset can be tokenized. That is becoming table stakes.

The harder question is what happens once those assets are onchain. Capital markets are not defined by asset ownership alone. They depend on financing, collateralization, liquidity management, and the ability to move capital efficiently through a system. The challenge is no longer whether assets can exist onchain. It is whether the infrastructure around them can make those assets productive.

The infrastructure decisions made now, where credit logic lives, how obligations are enforced, how risk is allocated, will determine whether onchain capital markets develop real depth.

The XRPL Lending Protocol (XLS-65, XLS-66) is subject to validator approval. Infrastructure providers and developers can begin integrating and testing on devnet today — see the Lending Protocol in action and help define how onchain credit markets take shape.